In Spanish, the word for retirement is jubilacion. However, whilst we might dream of the day when we can pack in our job and spend our remaining years travelling, spoiling the grandchildren and generally relaxing, the realistic prospect of such a jubilant future is looking less certain.

In the UK, this is due in part to the switch in pension schemes and working trends. Defined benefit pensions have been phased out due to the huge financial burden on companies caused by the increase in life expectancy. Over the last 30 years life expectancy at birth has increased by four hours per day for females and six hours per day for males, according to figures from the Office for National Statistics (ONS). On average women can now expect to live until they are 82.8, and men until 79. We have also seen the end of the 'job for life' ethos – people move jobs far more and may even have two careers in their working life.

In place of defined benefit pensions has come the defined contribution system which places all the burden of saving for retirement on the individual rather than the employer, just as in the US and Australia. Motivating ourselves to save for retirement is difficult though, due to a number of psychological barriers such as procrastination, inertia and the temptation to spend our earnings today rather than save them.

So it's no surprise, at least to behavioural scientists, that many people are failing to build up adequate retirement savings. In the UK, for example, a recent study found that people were putting just £2,500 a year into their pension, which would work out to around £450 per month, or £5,400 per annum in retirement. Given that most people expect to live off around £16,000 to £25,000 a year, at current trends most of us will fall a long way short of that, even when the state pension is factored in.[1] [2] Other figures are even more worrying – the Financial Conduct Authority found that current data suggests 50% of those approaching retirement have pension pots of less than £25,000.[3] (However, further analysis in the report suggests that pension pots make up only 12% of family wealth on average and on current trends, we might hypothesise that the rest is tied up in property.)

In this article, the final part of our three part series on personal financial management, we explore three issues around retirement saving from the perspective of behavioural science:

- Understanding the issue: How can behavioural science help to explain why people are not saving enough for retirement?

- Getting started: Can behavioural economics encourage people to save towards their retirement earlier in their working life?

- Increasing engagement: Finally, once a pension plan is in place, can behavioural economics help people to become more engaged and to save more, using concepts such as simple defaults, reframing, anchoring and priming?

We know that using simple tools from behavioural science can make a real difference to the savings people can potentially achieve. But first we need to recognise the psychological barriers to pension provision. Why is it that many of us are not saving enough for when we grow older? What are some of the psychological barriers?

We are generally optimistic, carefree procrastinators: The majority of us are optimistic about the future and probably take the view that it'll all work out in the end. For example, we might believe that we'll do well enough in our career to land a lucrative job or that we will one day win the lottery. Or we might take the view that one’s house is one’s pension, optimistically assuming the housing market will always go up and therefore feeling comfortable about putting all our eggs in one basket with no diversification. However, recent research indicates that downsizing your property may not release as much income as you might imagine. A recent Prudential survey of over-55s found that downsizing releases just £85,000 on average. That will buy you just £4,800 of annual income in retirement – not much huh? More worryingly, it assumes full ownership of a home, which may no longer be an accurate assumption with home ownership beginning much later in life now and 30 year plus mortgage terms becoming increasingly common.[4]

We also have a tendency to discount the future and live for today: Our behaviour can be influenced by a cognitive bias known as the 'power of now' or 'present bias', where we focus on what we'd like to enjoy now rather than later. So there can be an immense draw to spending our money now, further influenced by impulsive, emotional decision-making; and pensions can seem a dull, complex subject which require rational, thoughtful decision-making. So it's hard for pensions to compete with potential purchases today – such as travel, exciting events or glamorous material purchases – which are often dictated by more emotion-led decision-making. It certainly would seem far more appealing to take your family on holiday to the Bahamas, or organise a jaw-droppingly glamorous wedding than lock money away for when you’re old (a decidedly gloomy prospect). We also often suffer from a 'do it tomorrow' syndrome for things that need concentrated thought, so we are very likely to procrastinate and put off difficult, complex decisions. We may well know that we need to set up a pension or increase our contributions, but there always seems to be something more immediately important to do – so we push the decision back…and back. We may also be aware that it is an important subject, and a decision where we should carefully research all the information and consider all our options. In delaying action, we severely limit how much we are able to save up. Those who start to save early reap the benefits of compound interest over a longer time period.

We struggle to imagine our future selves: It's hard to conceive of what retirement might be like – what will we want and need? What will our tastes and preferences be? And because we struggle to imagine the kind of person we will be when we are old, it’s difficult to save for that person. Related to this is what psychologist Daniel Gilbert calls the 'end of history' illusion: We suffer from the illusion that we will remain exactly how we are today. It's difficult to believe that we will change from the people we are today and that we might want and prefer different things when we are old. Instead we generally live inside a fantastic illusion that we have just recently become the people that we were always meant to be and will be for the rest of our lives![5]

Wired: to save or not to save: Certain genetic dispositions mean that while some of us are born with an ability to save and plan for the future, apparently able to put money aside effortlessly, who never seem to 'want now' and have strong levels of self control, and there are those who find spending so 'painful' that they also have no problem saving. However, a proportion of us are wired to spend for today; we procrastinate or have poor self-control and it is this personality type who may often struggle to save for when they are older. (See our previous article "Save More Money in Four Easy Steps" for more on this.)

With these psychological barriers to retirement saving in mind, let's look at the ways in which behavioural science can help develop tools to counter them.

1. Getting started with a pension using nudging and steering behaviour:

One of the biggest barriers to paying into a pension is getting around to setting it up in the first place. Pension providers and employers typically take the rational approach that 'if we offer it, they will save'. Yet, the majority of people don't. Due to procrastination and a 'do it later' attitude, or perhaps more seemingly urgent financial needs, many people never get round to opening a stakeholder pension. It can also seem a complex decision – which provider should I choose? How much should I contribute? And into what (shares, bonds etc)? - so people often delay their decision until a later date when they believe they will have more time and energy. Unfortunately, this can have a deleterious impact on savings later in life.

But, following in the footsteps of Australia, the UK has begun automatically enrolling all employees into a workplace pension. Employees are automatically 'opted in', but can choose to opt-out if they prefer. Introduced in 2012, this is in the process of being phased in across all employers in the UK over the next 4 years. So far, the scheme has shown promise, particularly for younger employees. Opt out rates among 16 to 30 year olds are under 5% and overall stand at 7%.[6]

This move to auto-enrolment has been based on insights from behavioural science. Back in 2001, behavioural economists Brigitte Madrian and Dennis Shea examined data from a large US corporation and found that auto-enrolment raised enrolment into 401(k)s from 49% to 86%.[7] Similar studies on auto-enrolment have also raised participation rates to over 90%.[8] Behavioural science has found that defaults can be a powerful way to determine behaviour - we tend to stick with what has already been chosen or done for us and only the minority opt out. For example, organ donor registration is around 90% or more when people are automatically opted-in compared to just 20-30% when people must opt-in themselves.

These findings have influenced legislation in the US; the Pension Protection Act of 2006 encourages employers to offer auto-enrolment in workplace pension schemes. Employees are automatically enrolled in a savings plan unless they choose to opt out. Companies that utilise auto-enrolment have higher employee participation rates than those offering retirement plans without auto-enrolment. Participation rates are estimated to be 10 percentage points higher in plans with auto-enrolment (77%) than those without it (67%) according to a recent study.[9]

2. Increasing engagement in pensions using tools from the behavioural sciences

a) Clever defaults for pension consolidation

Defaults can not only be useful for the area of enrolment in retirement planning, but also useful in other areas such as merging and consolidating several pension pots into one to make the most of what you have. In today's working world people tend to move jobs relatively frequently, which often means that they end up with a number of pensions they have saved into at different times. Experts recommend that people consolidate these different funds into one single pot – it can reduce admin fees and make it easier to keep track of how much has been saved. Yet the same reasons that prevent people setting up a pension in the first place are also the reasons for failing to consolidate them. Moving jobs is stressful enough as it is and merging pensions typically falls quite low down on an employee’s priority list, if it appears at all.

Auto-consolidation can be a good solution. The Australian government found that although everyone had a workplace pension - 'a superannuation' - people were failing to consolidate their accounts as they changed jobs because it was not automatic. At its peak Australia had 30m accounts, but 8-9m were declared 'lost accounts'. To solve this Australia changed its legislation to an automatic 'pot follows member' set up – a simple default to help people manage their retirement savings most effectively. Now the UK has switched to auto-enrolment it may also face the same problem and is currently considering various solutions for consolidation.

b) Tools to increase savings rates automatically over time: When employees are automatically enrolled into a pension, choices about how much to contribute and into what also need to be autonomised. Which means more defaults. These are typically set at a low, less-than-ideal contribution rate – just 2 to 3% of an employee’s salary - too low to be able to offer a good source of income during retirement.

Behavioural economists Shlomo Benartzi and Richard Thaler have looked at how to boost people's contribution rates. On top of the psychological barriers already discussed, they realised that one of the main barriers to increasing contribution rates is the behavioural economic concept called loss aversion. People get used to a certain level of take-home pay and the downside to increasing their pension contributions is that they will face a reduced net income – something which seems particularly undesirable and can put people off saving more today.

To combat this mindset Thaler and Benartzi devised a way of allowing employees to pre-commit to increasing their contributions automatically on the advent of their next pay rise. Under this model – known as auto-escalation or Save More Tomorrow - an employee would still enjoy the boost of increased take home pay, even though a portion of it was being siphoned off into their 401(k). They designed a scheme where, in the first year, contributions would be raised to 6.5%, 9.4% in the second year, then 11.6% and finally 13.6% by the fourth year. Employees were always allowed to opt-out if they desired. The scheme was tested across different companies with DC pension schemes across the US.

After 4 years, their results were incredibly positive:

- 78% of those offered auto-escalation joined;

- 80% remained in the scheme through the fourth pay raise; and

- the average savings rates for participants increased from 3.5% to 13.6% over the course of 40 months.

The model behind Save More Tomorrow is becoming increasingly widely adopted - over 50% of employers in the US now offer it. A survey in 2010 by Hewitt Associates found that 6 out of 10 employers offered auto-escalation and of those who did not many said they were considering offering it.[10] Like auto-enrolment, this has been aided by the Pension Protection Act of 2006 which also allows employers to 'auto-escalate' employee pensions. Employees retain the right to opt out of either the enrolment or the contribution escalation.[11]

Interestingly, Benartzi has also found that the default contribution rate made no difference to employees' opt-out rate from a pension scheme - whether it was set at a 3% or 6% contribution rate for example. A frequent worry among pension providers and policymakers is that people might opt out of a pension scheme entirely if they don’t feel they can afford to contribute at that rate. Yet employees were not put off by a higher default savings rate to the extent that they would choose not to save and participation rates were still near 100%. Which simply illustrates the extent to which we are happy to stick to the status quo. We often stick to the default because we believe that someone more expert and authoritative than ourselves has recommended it.

Beyond automatic features and defaults though, behavioural science can offer several more useful insights and tools to get people saving more.

c) Priming higher contributions with new reference points

Creating new reference points – also known as anchors by behavioural economists - may be useful. Our decision as to how much to contribute to a pension is both consciously and subconsciously affected by the numerical reference points we are provided with.

Preliminary research by behavioural economists James Choi, Emily Haisley and colleagues have shown how low contribution rates can be nudged upwards by including cues for higher rates in emails to employees. An email to employees which included the statement 'You can contribute up to 60% of your income in any pay period' boosted contributions by 2.9% of income one month later for those who were contributing $2500 or less during the year.

For example, an employee contributing just $100 per month with a take home income of around $1700 per month, might have raised their contributions by as much as $50 in one month.[12]

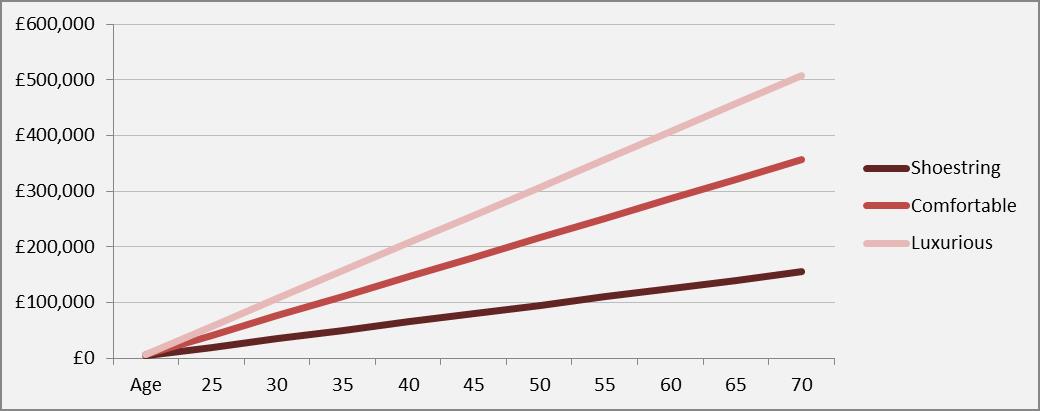

d) The power of extremes to increase contributions:

Another specific type of anchoring, known as extremeness aversion has also been found to be effective in steering behaviour. We tend to anchor to extremes and pick the middle option as a compromise. Pension providers could leverage this in annual statements and other communications they send by illustrating to employees what sort of lifestyle they are on track to enjoy in retirement and perhaps positioning lifestyles as one of three possible paths:

- shoestring

- comfortable

- luxurious

Providers may well be able to nudge savers currently on track for a spartan sounding 'shoestring' retirement upwards with communications such as 'You are on track for a 'shoestring' lifestyle in retirement, but could attain a 'comfortable' lifestyle by saving just £50 more per month!'. This could be further facilitated by visuals and plotting projected savings such as the example shown in the figure below.

e) Rules of thumb for saving

Shoestring retirements may in part be due to the advent of defined contribution pensions, because many people may not really know how much they need in retirement. According to an online survey carried out by Nest, the new UK pensions institution, happiness can be achieved at £15,000 a year or more. Below this figure, their research showed that retired life was too much of a struggle to be worry-free.[13] Financial advisers often quote that we need around two thirds of our current salary as income in retirement as a simple rule of thumb. Others suggest multiplying your desired annual income during retirement by 25 to give you a figure for the lump sum you need to have saved by the time you retire.[14]

But what do people need to save each month to attain that minimum? Those rules of thumb leave people with a lot of maths to do to work out how much they need to be saving each month. Numerous online pension calculators help with this, but it can still be a confusing area, with various assumptions on rates of return and inflation. People will be most engaged if they can see directly and immediately what saving now might mean in terms of monthly or annual income in retirement. Easy to use pension calculators should be the method of choice to make the projected monthly income most salient at the time of deciding how much to contribute each month.

f) Reframing retirement

How much we need to save for retirement is considerably affected by the exact age at which we retire. And due to increases in life expectancy, we are all going to have to work for considerably longer than our parents and grandparents did in order to balance out the spending period with the saving period. Children born in 2014 are forecast to have to work until they are 77. And PwC forecasts that children born in 2050 will need to work until they are 84. Many people are unhappy about this prospect. But is this simply because we are anchored to the idea of retiring at 60 like our parents did?

To buffer this, we can use the concept of reframing information in order to present it in a different light. For example, we could reframe retirement ages, perhaps by proportions of our lifetime. Many people are now spending longer in education and starting work later, and we are also living much longer, so the proportion of our lifetime that we spend in retirement is actually still roughly the same.

Retirement might also be reframed as a chance for you to focus on what you want to do with your later life, when you no longer need to look after your family and be the breadwinner. Instead, it can be a chance to focus on a lifetime hobby or even a new career. This could be a motivator to get people to contribute more into their pension and is an idea which Prudential has recently drawn on in its 'Bring your challenges' campaign.[15] Taking a number of case studies of recent retirees in the US, they reframe retirement as a time to do what you love, giving it a far more positive and appealing spin as a time of life that would be much more motivating to save for.[16]

g) Reframing contributions and savings

We can also reframe the act of paying in pension contributions. It may feel like paying money into a pension is saying goodbye to it forever. Many people find the idea of locking money away for decades a little alarming, it's painful to pay out money with only a very distant prospect of getting something in return. The money paid into an invisible pension can seem much more relevant for now. What if I need it for an emergency? What if I need to help out my children or pay for important medical treatment? It may feel like there is no gain, and might seem like money lost. But can those payments be reframed by a simple change in language?

One American employee, Jenine Holmes writes of how she learned to rethink her pension contributions as paying herself rather than the taxman:

"If you sock some of your savings into a SEP IRA account," my accountant advised, "you’d reduce your tax liability." With that I learned to make saving for retirement into a hedge against a higher tax bill, while creating a foundation for my future. My deposits ranged from $5,000 to $10,000 each year for three years. Sure, it hurt. But as Wendy my accountant asserted, "It hurts less to pay yourself, right?"[17]

Another idea for employees in the UK is to reframe the advantages of the tax benefits plus employer matching payments that come as part of UK pension schemes. A simple retail example (familiar to almost everyone) could do this: the Department for Wo rk and Pension adverts say: “You put in £40, your boss puts in £30 and you get £10 tax relief. £40 becomes £80.” This can be simply reframed or anchored to a type of 'buy one get one free'[18] or 'double your money' concept, people see them in supermarkets or the slot machines every week.

rk and Pension adverts say: “You put in £40, your boss puts in £30 and you get £10 tax relief. £40 becomes £80.” This can be simply reframed or anchored to a type of 'buy one get one free'[18] or 'double your money' concept, people see them in supermarkets or the slot machines every week.

Reframing might also be useful to avoid what behavioural economists call the ‘illusion of wealth’ - thinking we have saved more than we really have. Behavioural scientists Shlomo Benartzi, Hal Hershfield and Dan Goldstein carried out research which demonstrates that seeing the lump sum saved (so far) in their annual pension statement can lead people to suffer from ‘illusion of wealth’ issues, luring them into thinking they have a considerable amount of money saved. A lump sum of £100,000 can seem like a lot to someone mid-career, earning an average salary, and may lead them to rest on their laurels, even though it is not enough to fund a retirement.

Benartzi and his colleagues tested ways to counter this effect in a field experiment run in conjunction with a financial advisory firm. Financial advisers phoned 139 of their clients and told them how much money they had saved - either as a lump sum or in terms of what that sum would roughly equate to as their projected monthly income in retirement. They then asked them if they would like to change their current savings rate and if so, what that new rate would be. 36% of people who were quoted the monthly income figure opted to increase their savings, compared to only 21% of the lump sum group. In addition, those quoted the monthly income figure increased their savings rate by more than those quoted the lump sum figure.[19]

So annual pension statements which show the lump sum saved up front on the cover page may actually work against encouraging people to save more. In fact the lump sum expression of pension funding may prompt them to reduce or stop payments, or, even worse, cash them in, believing they have more than enough. Benartzi, Hershfield and Goldstein recommend that the projected monthly income be presented first in a statement, so savers can anchor to this and easily compare it to their current salary or income. This would make it salient and show immediately if the amount they have saved so far is not enough and hopefully prompt action.

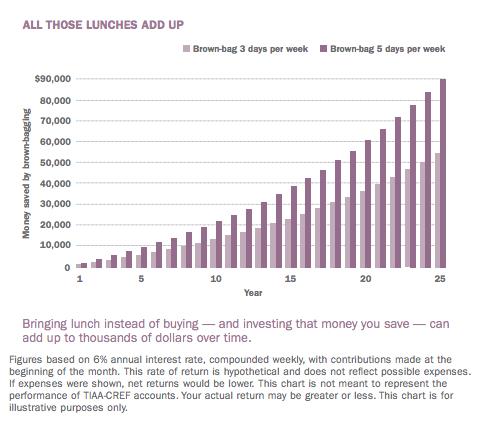

Finally, we can also find ways to save just that little bit more each month, something that can make a real difference in the long term due to compound interest effects. For example, the US pension provider for teachers and those in academia, TIAA-CREF, visually frame and illustrate the compound effects of ‘brown-bagging’ (bringing sandwiches in from home) two days a week instead of always buying lunch out.[20] Helping people to make simple, concrete plans to save more money and making that plan visually salient and appealing can go a long way to boosting retirement income. Pocket that saving into your retirement fund for 25 years of your working life and it could mean a difference of tens of thousands of pounds to your lump sum of savings.

Last thought - Would new British pensioners really blow their pension on a cruise?

One last thought for when you get your pension in the UK… From April 2015 all restrictions on access to pension funds will be removed. British retirees will be allowed to access their pension as one lump sum rather than having to buy the more traditional annuity. This move has led to a debate about whether retirees might impulsively throw their pension away on a luxury cruise or something else frivolous once they begin retirement.

It’s true that this might be the case for some, due to impulsivity, the power of now and the temptation to spend. However, with pensions now defined contribution (self-managed) rather than defined benefit (provided to people by their employer), behavioural economic concepts such as the endowment effect and loss aversion are likely to have an impact, as people who have worked hard to save up a lump sum for retirement over their lifetime struggle with the idea of spending a large chunk of it frivolously.

Conclusion

We have seen here that behavioural science has real power to change people's future retirement prospects for the better – from simple defaults like auto-enrolment to get people starting to save, or auto-consolidation or auto-escalation to boost savings, to tools and techniques such as reframing information and using new anchors and reference points to encourage people to save more.

We should celebrate these simple, virtually costless techniques which can help the vast majority of us save a little more and make our retirement a brighter, more jubilant one.

Read more from Crawford.

[1] Thisismoney.co.uk “The great British pension chasm: Millions face stark choice of working into old age or surviving on far less than they think” 29th July 2014

[2] The current basic state pension is £113.10 per week. From April 2016 this will increase to £148 per week in today's money under the new flat rate system.

[3] Financial Conduct Authority “Pension Annuities: Review of Consumer Behaviour” January 2014

[4] Financial Times ‘Nest’s pension price may not be right, but it’s a start’ 23rd May 2014

[5] Quoidbach, J., Gilbert, D.T., Wilson, T.D., ‘The End of History Illusion’ Science, Vol. 339, 4th Jan 2013

[6] Financial Times, ‘New UK pension flexibility might backfire’ 13th April 2013 and ‘Pensioner poverty fears grow for over-50s’ 28th January 2014

[7] Madrian, B. Shea, D.F. “The Power of Suggestion: Inertia in 401(k) Participation and Savings Behavior” 2001, Quarterly Journal of Economics, 116(4): 1149-1187

[8] Choi, J.J., Laibson, D., Madrian B.C., and Metrick, A. “Defined Contribution Pensions: Plan Rules, Participant Decisions, and the Path of Least Resistance” NBER Working Paper No. 8655, December 2001

[9] Butrica, B.A., and Karamcheva, N.S., “How does 401(k) auto-enrollment relate to the employer match and total compensation?” Oct 2013, Center for Retirement Research at Boston College. Analysis of Bureau of Labor Statistics data.

[10] AON Hewitt Associates ‘Hot Topics in Retirement 2010 - Survey Findings’

[11] Thaler, R., Benartzi, S., “Save More Tomorrow: Using behavioral economics to increase employee savings”, 2004, Journal of Political Economy 112.1, Part 2, pp S164-S187

[12] Choi, J.J., Haisley, E., Kurkoski, J., Massey, C. “Small Cues Change Savings Choices” NBER Working Paper No. 17843, June 2013

[13] Financial Times ‘Nest’s pension price may not be right, but it’s a start’ 23rd May 2014 and Nest “Retirement Realities: Retirement’s Worth Saving For” 2014

[14] This rule of thumb makes the reasonable assumption that you retire at 65 and live until you are 90.

[15] Prudential, Bring Your Challenges: www.bringyourchallenges.com. In their 'Challenge Lab' they tackle some of the barriers to retirement saving (I'll do it later, It won't happen to me etc) offering behavioural science expert Dan Gilbert's analysis of how best to overcome them.

[16] See Chapter 2 of Prudential’s recent ‘Bring your Challenges’ campaign, www.bringyourchallenges.com

[17] LearnVest/Jenine Holmes “How I rebooted my Retirement Savings after 40” 13th Aug, 2013

[18] Financial Times ‘Nest’s pension price may not be right, but it’s a start’ 23rd May 2014

[19] Goldstein, D.G., Hershfield, H.E., Benartzi, S. “The Illusion of Wealth and its Reversal” 2014

[20] TIAA-CREF Life Goals Series ‘Saving for Retirement’

www1.tiaa-cref.org/ucm/groups/content/@ap_ucm_p_tcp/documents/document/tiaa01007923.pdf